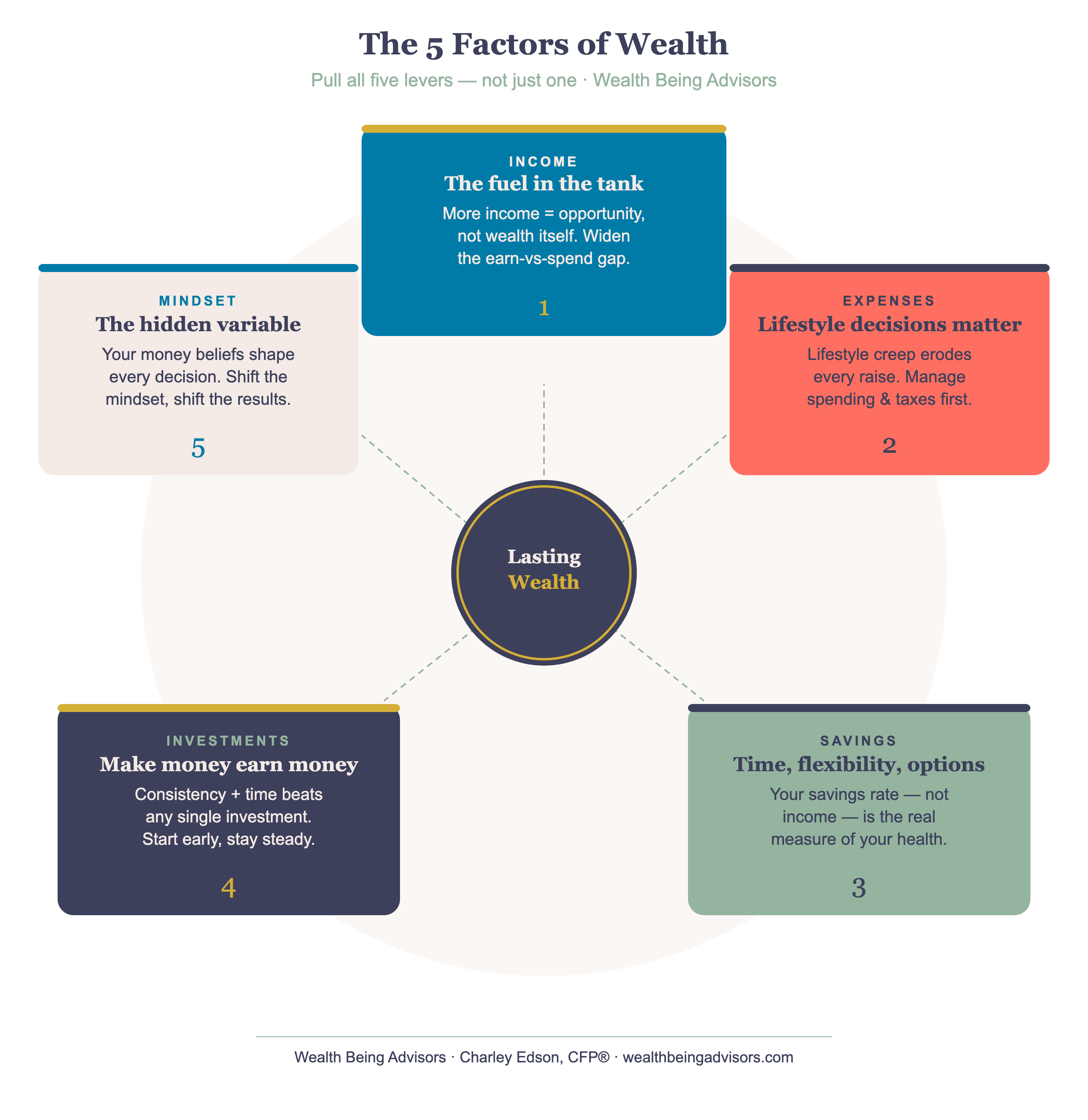

The 5 Factors That Actually Build Wealth

A high income doesn't guarantee wealth. Here are the 5 factors that actually drive wealth building for high earners and where most go wrong.

Most People Think Growing Wealth Is About Investing. It's Not.

If you're a busy professional earning $200,000 or more, you've probably been told that the key to wealth is investing. Max your 401(k). Pick the right funds. Let compound interest do the heavy lifting.

And while investing matters, and it absolutely does, it's only one piece of the puzzle. In over a decade of working in finance, I've seen high earners make this mistake repeatedly: they focus intensely on one lever while the others quietly work against them.

It’s like trying to pump gas into your car when the gas station is dry.

The result? A six-figure income and net worth that doesn’t grow.

The truth is, growing your wealth is driven by five interconnected factors. When you neglect or don’t focus on even one, you're at risk of throwing off the entire wealth engine.

Below are the 5 wealth growing factors.

💵 Factor 1: Income, The Fuel in the Tank

Income is the starting point. It's the fuel that powers everything else. Without it, the other four factors have very little to work with.

Where most people go wrong is thinking more income alone means more wealth. While income is the fuel for driving your wealth, where you put it determines what direction your wealth will go. Will you decide to put it in things that will grow your wealth (investing & saving), or spend it?

💡 Optimization Tip: Focus not just on growing your income, but on widening the gap between what you earn and what you spend. That gap is where wealth is actually created.

Pro tip: Have a dedicated, separate checking or savings account where you funnel all income to. Don’t let this be the account you pay your bills from.

🧾 Factor 2: Expenses, Your Lifestyle Decisions Matter

Expenses are wealth killers. Every dollar you spend is a dollar that doesn't compound, doesn't invest, and doesn't build toward your future. And for most high earners, expenses are the most underestimated wealth killer of all.

Lifestyle creep is real and it's devastating.

According to a 2025 Forbes analysis, roughly one-third of Americans earning $200,000 or more still live paycheck to paycheck.

Here's how it happens: You get a raise, so you lease a nicer car. You land a big client, so you upgrade your home. These aren't irrational decisions. However, each one raises your baseline spending floor permanently. Over time, that rising floor consumes the very income growth that was supposed to build your wealth.

I talk more about lifestyle creep in this article link.

And then there's the expense most people underestimate: taxes. For someone in a high income bracket, taxes can be one of the single largest annual expenditures. This is why strategic, legal tax reduction isn't just smart for long term wealth building, it's essential. Every dollar in unnecessary taxes paid is a dollar that never had the chance to compound.

💡 Optimization Tip: When income rises, resist the urge to upgrade everything simultaneously. Automate a portion of every raise directly into savings or investment accounts before lifestyle spending has a chance to claim it.

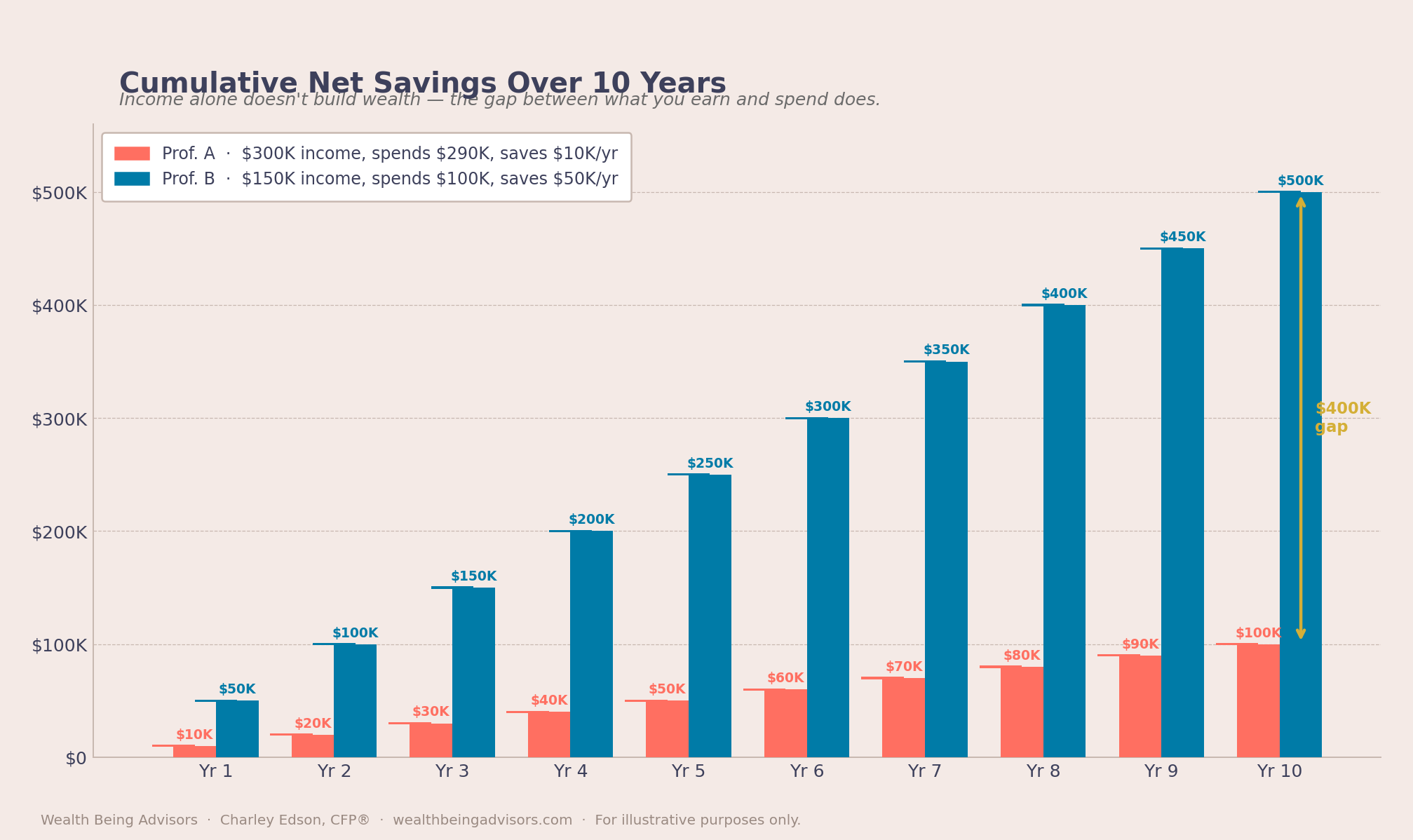

🏦 Factor 3: Savings. Time, Flexibility, and Peace of Mind

Savings are your income minus expenses. You can manipulate either side of the equation to increase your wealth building capacity!

Let’s walk through a quick scenario.

- Professional A earns $300,000 per year and spends $290,000.

- Professional B earns $150,000 per year and spends $100,000.

Who would you rather be?

At first glance, maybe you say Professional A. But Professional B is actually building $50,000 in net savings annually, compared to Professional A's $10,000. Over a decade, that difference becomes very large. Without compounding, it is $500,000 versus $100,000. Is the choice clearer now?

According to the Federal Reserve's 2025 Report on the Economic Well-Being of U.S. Households, only 55% of U.S. adults have at least three months of expenses in emergency savings. For high earners, a robust savings buffer also provides something else: the freedom to take calculated risks. Whether that's investing in a business, negotiating a career move, or simply not making fear-based financial decisions.

Savings are often misunderstood as simply a financial safety net. But they are far more than that. Savings buy you time, flexibility, and options. These become increasingly valuable as your career and life grow more complex.

For high earners aiming to build their wealth, it is recommended to try and save 20% of your net income. Especially during peak earning years when both income and compounding potential are at their highest.

💡 Optimization Tip: Think of your savings rate, not your income, as the true measure of your financial health. The gap between income and expenses is your real wealth-building engine.

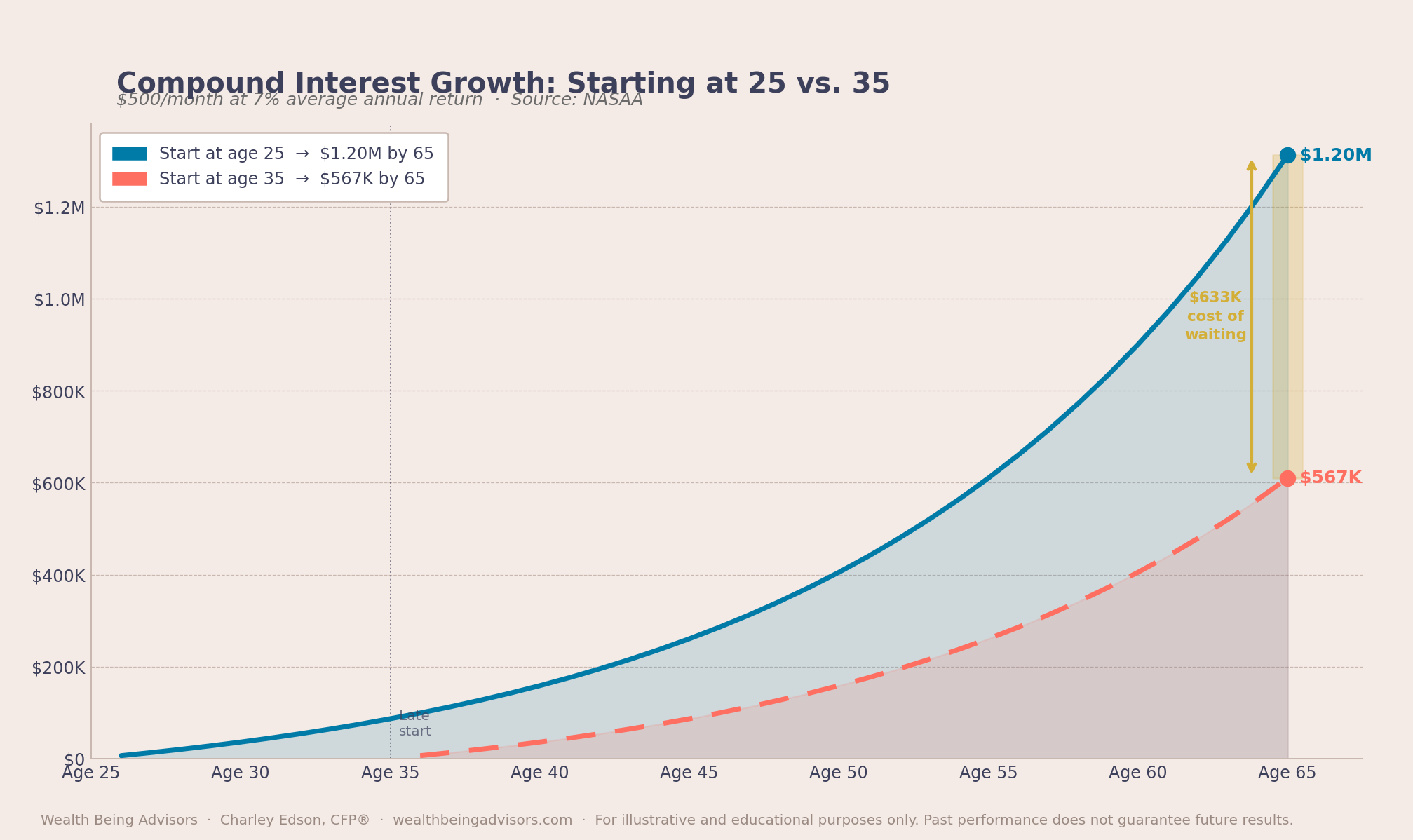

📈 Factor 4: Investments. Putting Your Money to Work

This is the factor most people fixate on, and for good reason: investments are how your money earns money. It's how you scale wealth beyond what income alone can provide.

The principle is beautifully captured in a quote often attributed to Albert Einstein:

"Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn't, pays it."

Here’s another example. According to NASAA, a 25-year-old who invests $500 per month at a 7% average annual return will accumulate approximately $1.2 million by age 65. A 35-year-old doing the exact same thing ends up with roughly $567,000. Less than half. Simply because they started a decade later. Time is the most powerful compounding variable there is.

But here's the critical piece: investments only work powerfully when the first three factors are already functioning. When income is unstable, expenses are unchecked or unclear, and savings are insufficient, it doesn’t allow you to add fuel to the fire. You can’t compound with $0. Your ability to save allows compounding to work, and allows your money to earn more money. This is why you need to take a careful look at each factor above, before thinking about investments. If you don’t, you may need to pull money out of investments to pay for expenses not planned.

💡 Optimization Tip: Don't wait for the "perfect" investment. Consistency and time in the market, driven by a strong savings rate, matter more than any individual investment decision.

Note: All investment examples above are for illustrative and educational purposes only. Past performance does not guarantee future results. Consult with a qualified financial advisor before implementing any investment strategy.

🧠 Factor 5: Mindset. The Hidden Variable That Controls Everything

Mindset may be the most underrated factor in this entire framework. It affects all the others, perhaps more than any single factor.

Your beliefs about money, whether you're aware of them or not, shape every financial decision you make. These are called your money blueprint. They influence how freely you spend, whether you prioritize savings, how you respond to market downturns, and whether you engage actively with your finances or avoid them altogether.

For many high earners, a fixed or scarcity-based money mindset can manifest in surprising ways:

- Avoiding looking at account balances out of anxiety

- Spending freely because "there will always be more"

- Underinvesting because markets feel uncertain or risky

- Procrastinating on financial planning because it feels overwhelming

A growth-oriented financial mindset, on the other hand, treats wealth as a skill to develop, not a destination to arrive at. It embraces learning, welcomes delegation to experts, and makes proactive decisions rather than reactive ones.

This is perhaps the most subtle of the five factors. However, when you shift it, you tend to see the most dramatic improvements across all the others.

💡 Optimization Tip: Audit your money beliefs. Ask yourself: "What story am I telling myself about wealth?" The answers often reveal where your financial blind spots are hiding.

🎯 Wealth Is Built When All Five Work Together

Most people focus on one or two of these factors. Usually income and investments. But the professionals who build lasting, meaningful wealth are the ones who understand that all five levers must be intentionally managed at the same time.

Here's what that looks like in practice:

✅ Income grows through career development, entrepreneurship, or additional revenue streams.

✅ Expenses are managed strategically, especially taxes, to preserve as much income as possible.

✅ Savings create a buffer and a wealth-building engine through a high savings rate.

✅ Investments put those savings to work with the power of compounding time.

✅ Mindset keeps you engaged, intentional, and resilient through every financial season.

Pull all five levers, and your financial trajectory changes dramatically. Ignore even one, and you may find yourself earning more than ever while wondering why wealth still feels out of reach.

Ready to talk it through?

Book a complimentary 30-minute conversation with an advisor.

Schedule a meeting →Sources

- The Massive Cost Of Lifestyle Creep And How To Avoid It — Forbes (April 2025)

- Report on the Economic Well-Being of U.S. Households in 2024 — Federal Reserve (June 2025)

- How Much Should You Save to Achieve Your Financial Goals? — Curi Capital (June 2026)

- Compound Interest — NASAA

- Average and Median Net Worth by Age — NerdWallet (June 2026)

Frequently asked questions

Q: What is a money mindset and why does it affect wealth?

Your money mindset is the set of beliefs you hold about money — whether you're aware of them or not. They shape how freely you spend, how consistently you save, and whether you engage with your finances or avoid them. A fixed or scarcity-based mindset quietly works against every other factor. Shifting it tends to create the most dramatic improvement across the board.

Q: Where do I start if I want to get all five factors working?

Start with clarity. Know what's coming in, what's going out, and what the gap is. From there, automate savings before spending has a chance to claim it, then let investments do the compounding work. A financial advisor can help you build the structure so you're not managing it all manually.