More Money Won't Fix This

The Cash Flow Engine: Turn Your Income Into Lasting Wealth

TL;DR

- Making more money won't get you to financial freedom faster. What you do with it will.

- Saving fails because spending is the default. Our paycheck lands in an account designed to spend. Willpower was never the problem.

- The Cash Flow Engine flips the default: income lands in savings first, checking gets a set amount, and the excess intentionally buys assets.

- Assets grow and compound whether or not you show up for work and eventually, they can pay you.

- In a hypothetical 30-year projection, the same paycheck built $6.9M with the engine vs. $2.2M without — a $23,050/mo retirement paycheck vs. $7,193. The difference is the system.

More money won’t fix this

“How can I make more money so I can retire earlier?” This is the number one thing I hear in one form or another from clients, prospects, and friends when we talk about money.

This is then inevitably followed by: “If I just earn more, I’ll be set.”

Then they start listing ways they can earn more: side hustles, a second job, working more, starting a business.

To me, the real question they are asking is, “How do I grow my money and know when I can stop working?”

Making more money doesn’t fix any of that.

In reality, a lack of structure and a plan is an easy path to anxiety. It is also an easy way to let current and future income slip into unintentional spending and push financial freedom further away.

To quote Noah Kahan “Who likes living, just to die.” Life is meant to be enjoyed and not spent working all the time.

There is a simple, sustainable, and repeatable way to create clarity and reach financial freedom.

I hate the term passive income

I say that tongue and cheek. Passive income is great, but it isn’t the focus.

Assets are expected to grow in value over time. They also can have the ability to generate income for you.

Real estate income, dividends, interest, business interests, are all forms of what is called “passive income”.

These are what allow you to live off of your money (financial freedom) without having to rely on active income.

Make enough of it and know how much you want to spend? You have the answer to your question.

But hold up. Before we can think about that, we’re missing a few steps. It’s like saying you want to get in shape and buying a gym membership, but never going. We missed the process, we missed the structure. Scheduling time to go, making it easy, dialing in our nutrition, etc.

We also missed what the end goal was and why we wanted it in the first place. Where is the purpose? Do you want to continue playing sports for fun pain free? Do you want to be healthy as you age?

Same with money. When do you want to stop working? What will you do when you stop? Do you want to take a less demanding job that you’ll enjoy more? All of these change the calculus.

The goal of passive income is nice to fund your lifestyle, but the way we get there is so much more important. The system.

Don’t focus on generating passive income. Focus on the system.

So let’s work backwards from the goal.

Passive income comes from buying assets.

But where does the money to buy them come from?

Why is it so hard to save?

Before we can buy any assets and generate income, we need to take our income and subtract our living expenses. This is our net cash flow, and we get to decide what to do with it. We either A) intentionally spend it or B) buy assets that move us toward financial freedom faster.

Unfortunately for us, the world is set up to make this an uphill battle. For most people I talk to, direct deposits from their job or business land in their checking account.

Why does this hinder our ability to save?

Our credit cards are paid off from it. We Venmo our friends for dinner from it. Rent is pulled from it. Everything you spend money on is connected to this account. It should be called a spending account. It’s also difficult to track. All of which is why budgeting is hard.

When money comes into this account, it generally gets spent. If you are human like me, you struggle with this too. We have a set number we try to keep to, but no real system. Or no plan for excess money.

This isn’t our fault. The system is just set up for us to spend money. It is easier now than ever to open your phone and get hit with 30 ads from Insta, TikTok, or TV. It is hard fighting against corporations spending millions on the science to get you to spend money.

Behavioral economists like Richard Thaler have shown that people overwhelmingly follow the default option. We take the path that requires no decision (Nudge, Thaler & Sunstein). And the default path for your money is consumption. Lifestyle creep isn’t a flaw, it is designed. Companies count on it.

The good news? We can implement a system that stops this unintentional spending, flips the system on its head, and gives us back some power to direct our money. Yes it is a bit of work. No, it isn’t a magic bullet that will magically save you a bunch of money.

But it is a system you can actually implement. One that creates savings, uses savings to buy assets, and lets those assets generate income you can live on. Financially free.

The old way relies on willpower to not spend. It makes it easy to spend.

The new way relies on a system to save. It makes it harder to spend.

The system

Start by having your direct deposits, and any other income land in a separate savings account.

Then determine how much you need to live on. You can use this link to help plan your cash flow if you need to.

Take that number and multiply it by 3-6, depending on how many months you want in your emergency fund and how conservative you are.

That number becomes your benchmark. It will provide feedback on whether you’re overspending, or have extra cash to spend intentionally or buy more assets.

Next, automate the monthly amount you need to live on and send it from savings to checking each month to pay your bills. You can start off with 1-2 months of expenses in your checking to avoid overdraft.

This next part is important.

If your savings account is above the benchmark, because your income increased, or you spent under your budget, you can intentionally use that money and spend it, or buy assets to generate more income.

If your account is below the benchmark, then it’s your job to look at where your money went, and bring it back in line. You’ll most likely have to adjust your lifestyle expenses. The earlier you catch it, the smaller the correction.

As time goes on, this system lets you direct your income into assets, by repeating the loop over and over.

It is simple, but it isn’t easy. Yet, if you can follow this, it is the blueprint for growing your wealth.

Scenario: Same Paycheck, Two Different Paths

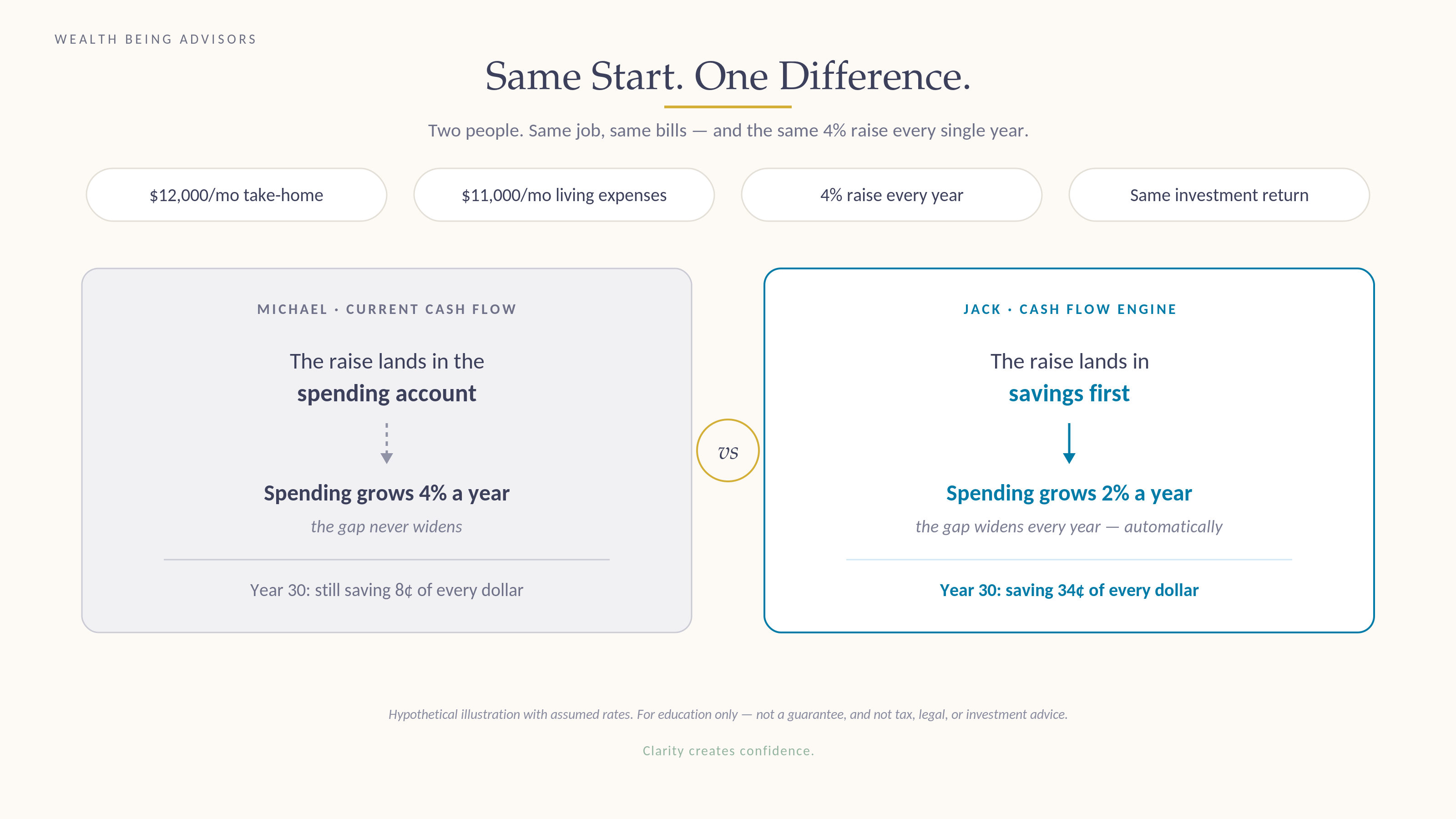

Meet Michael and Jack. Same job, same paycheck, same bills.

Both take home $12,000 a month. Both spend $11,000 a month living their life. Both save what's left, $1,000 a month, and invest it at the same return.

Both get the same raise, too: 4% a year, every year, for 30 years.

There is exactly one difference between them: what happens to the raise.

Michael: Status Quo. The raise lands in the spending account. So spending grows right alongside income, 4% a year, by default. The gap between what comes in and what goes out never widens. He saves the same slice of his income his entire career.

Jack: The System. The raise lands in savings first. His lifestyle still grows, 2% a year, still upgrades, just slower than his income. The gap widens every single year, and the system invests it automatically.

In year one, they're identical: both save about 8 cents of every dollar. By year 30, Michael is still saving 8 cents. Jack's system is now capturing 34 cents of every dollar.

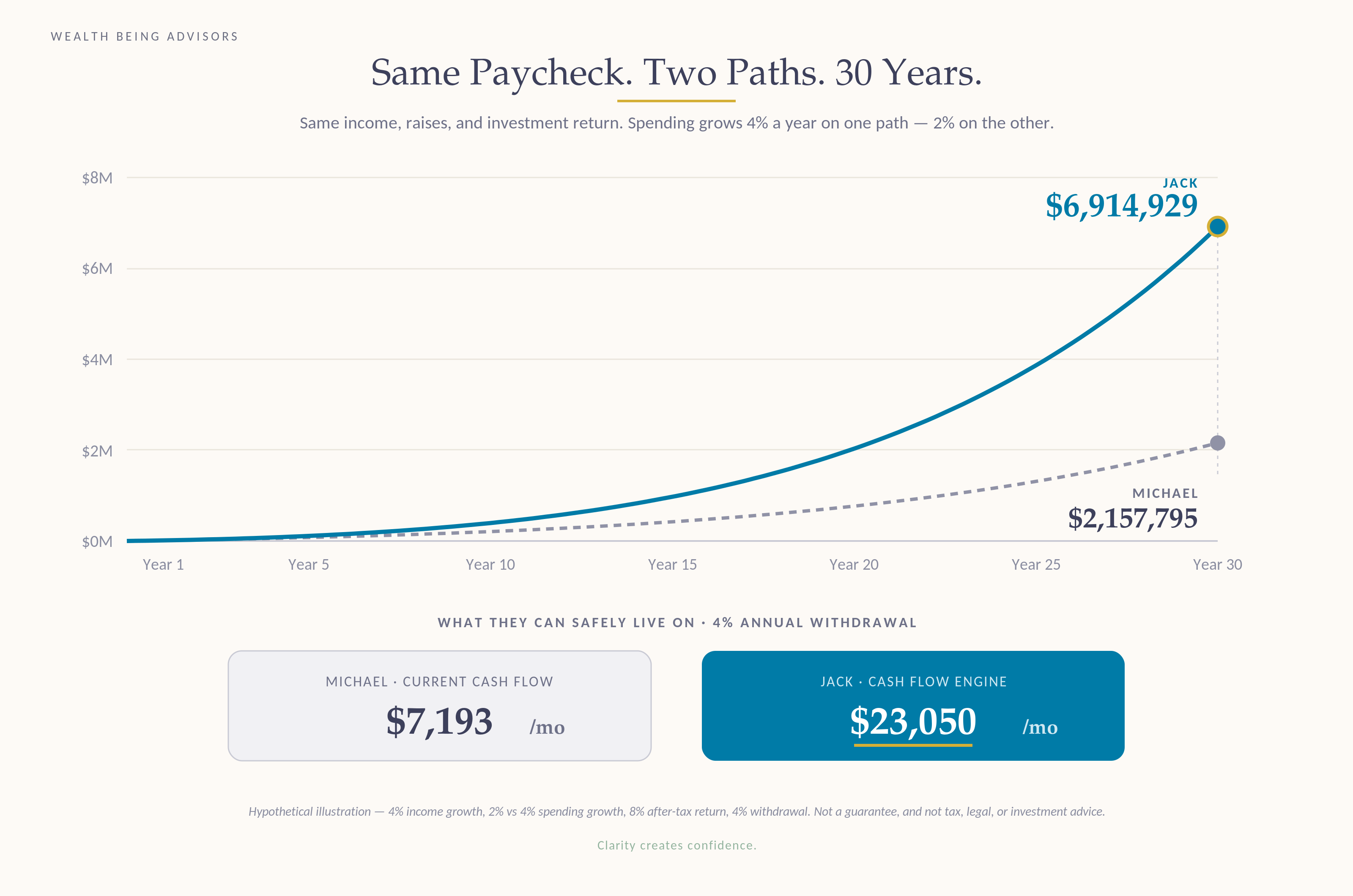

Here's where they land after 30 years:

- Michael's assets: $2,157,795

- Jack's assets: $6,914,929

More than three times the wealth. The paycheck, the raises, and the investment return didn’t change. The only lever that moved was how fast spending grew. In my experience, that lever moves the needle far more than chasing a better rate of return ever will.

Here is where I want it to hit home. Their financial freedom numbers are wildly different.

Using a 4% annual withdrawal, a common planning guideline for sustainable retirement income, here's the check their assets write them every month:

- Michael: $7,193 a month

- Jack: $23,050 a month

Think about that.

Michael's life costs about $35,700 a month. His assets pay $7,193. Thirty years in, he can't stop working, unless he drastically reduces his lifestyle.

Jack is able to stop his paycheck, and support is lifestyle and live financially free. That is the answer to his question.

Same job. Same raises. Same returns. Two different systems.

This is a hypothetical illustration with assumed rates — 4% income growth, 2% vs. 4% spending growth, an 8% after-tax return, and a 4% withdrawal rate. It's not a prediction or a guarantee, and your numbers will differ.

Why isn’t everyone doing this?

There are a few reasons why:

- I did say it is simple, but not easy.

- Humans also like the status quo, and this does take some work to set up.

- Waiting because you don’t feel you make enough, or aren’t in a good financial position.

- You still think making more money is the key and don’t need to waste your time.

The first one is why I’m in business. I help people do this for a living.

If you’re someone who doesn’t like change or doesn’t see anything wrong, hopefully the scenario above showed you something you haven’t seen.

I would argue the third is the exact reason why you should start now. The system doesn’t care how much you make, it just cares when you start. Small habits turn into huge differences over time.

If you are the fourth, well then good luck. Earning more works for a few people, but not consistently. More income without a system is just a bigger engine with the same leak.

A bigger engine with no leaks is where this really makes a difference.

Conclusion

Growing your income isn’t enough to help you reach financial freedom. It’s what you do with it that matters.

Intentionally directing your net cash flow to buying assets is a powerful tool for building wealth.

This isn’t set-it-and-forget-it. You review it monthly to ensure you’re on track. At the end of the day, nobody should care more about your finances and future than you do.

All it takes is one decision saying yes to your future self. Break the default mode. Set the system up once, and let it run.

Sources

- [Nudge — Thaler & Sunstein (for the default-option claim)]