Why a Savings Account is Not Safe

A high-yield savings account feels safe, but inflation risk quietly erodes your money. Here's when to save vs. invest for long-term wealth.

A friend recently told me she thinks of putting money into a high-yield savings account as "growing" it, while avoiding putting money in the stock market, because it “feels too risky.”

I've heard some version of this many times. A little part of me also dies on the inside every time I do. I genuinely get it and the psychology makes sense. A savings account shows a number that never goes down. Investing has days when it does. Which is scary. One feels safe, the other feels like going towards the lion trying to eat you.

The thing lurking below: inflation risk

However, there is a bigger, just as real risk lurking in the shadows of this decision, that is possibly an even bigger one.

And that is inflation risk. Inflation eating up the amount that money can buy in the future. Or said differently, you will be able to buy less things with your money in the future, than you can now.

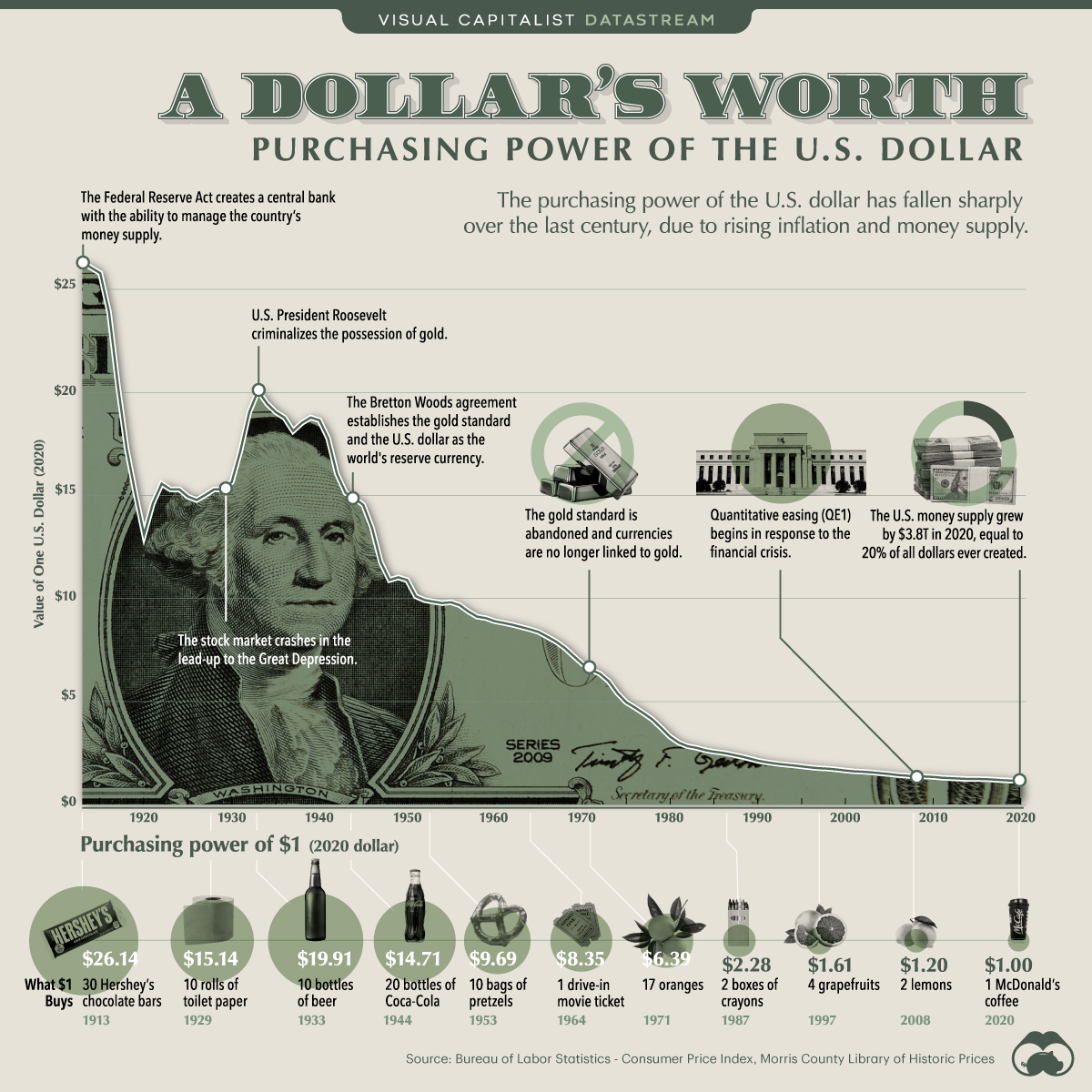

For example: Say lunch costs $15 now. Queue the “I remember when lunch only cost $10 remark from us aging millennials. Well it’s true. That is called inflation. If you put $10 into the stock market 10 years ago, it would be worth $29.54. If you put the same $10 into a HYSA, it would be worth $8.95.

You wouldn’t be able to buy lunch anymore.

Inflation risk is like an invisible leak on your money. You may not see it right away, but if you zoom out, it will show.

So what is stock risk?

How I define risk in the stock market is pretty simple. How much they move up or down. So what if I told you there was a way to reduce risk, or reduce the amount it goes up or down. What if I said it was actually pretty simple. However, don’t confuse simple with easy. In fact, some people find this incredibly difficult. Which is why insert value of a financial advisor monologue...

Ok sorry about that, where were we? Right ok.

The answer is time.

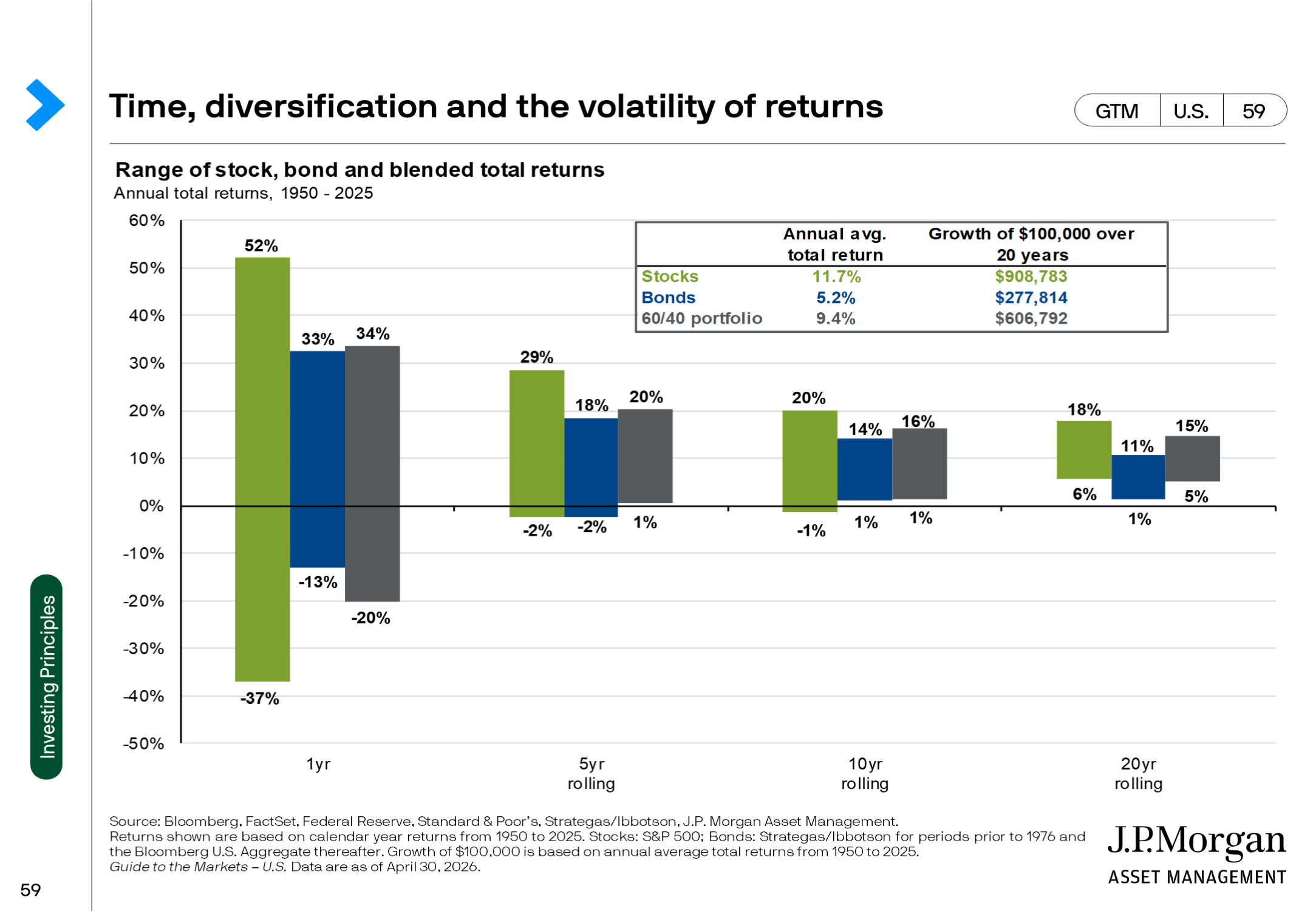

Consider the following chart by JP Morgan. All I want you to look at is the green bar, which represents the stock market.

Time is going from left to right. Returns are up to down.

Here is my takeaway:

Short term, markets are unpredictable.

Long term, we reduce our chances of losing money, and increase the chances of growing our wealth.

So when should we invest and when should we keep in savings?

To not beat up on HYSA too much, they do have merit. They are there in case of emergencies, and short term goals. That is how I use them for clients.

While it is subject to your unique case, generally if someone needs the money within 1-3 years, it may make sense to keep in savings. If you don’t and it is earmarked for the long term, you may be better served investing into the market to beat inflation over the long run.

The mindset for long-term wealth

The real enemy of long-term wealth isn't the market. It's our very human discomfort with uncertainty.

A savings account feels safe because the number doesn't move. But that's an illusion of safety, not actual security. Inflation never shows up as a negative balance. It shows up as the same $10 buying a lot less in ten years, and not even lunch!

Investing feels risky because the number does move. But that movement is the price of admission for returns that actually outpace inflation and make your money work as hard as you do.

Sources: https://www.visualcapitalist.com/purchasing-power-of-the-u-s-dollar-over-time/

Disclaimer: Charley Edson is an investment adviser representative of Wealth Being Advisors, a registered investment adviser. This content is for education and information purposes only and should not be relied upon as financial, investment, legal, or tax advice, nor is it intended to make any recommendation. All investing involves risk, including possible loss of principal. Past performance does not guarantee future results. All figures and scenarios are illustrative only. Consult a qualified adviser before making investment decisions.

The S&P 500 to approximate the market, and SHV (iShares 0-1 Year ETF) to approximate HYSA was used as in the lunch example.

Frequently asked questions

Is a high-yield savings account a good investment?

It's a good tool for emergencies and short-term goals (money needed within 1–3 years), but it typically doesn't keep pace with inflation, so it's not ideal for long-term growth.

What is inflation risk?

Inflation risk is the chance that the money you hold will buy less in the future than it does today. It doesn't show up as a falling balance — it shows up as your dollars stretching less far over time.